Last updated: July 25, 2025

What Is Gap Insurance and How Does It Work?

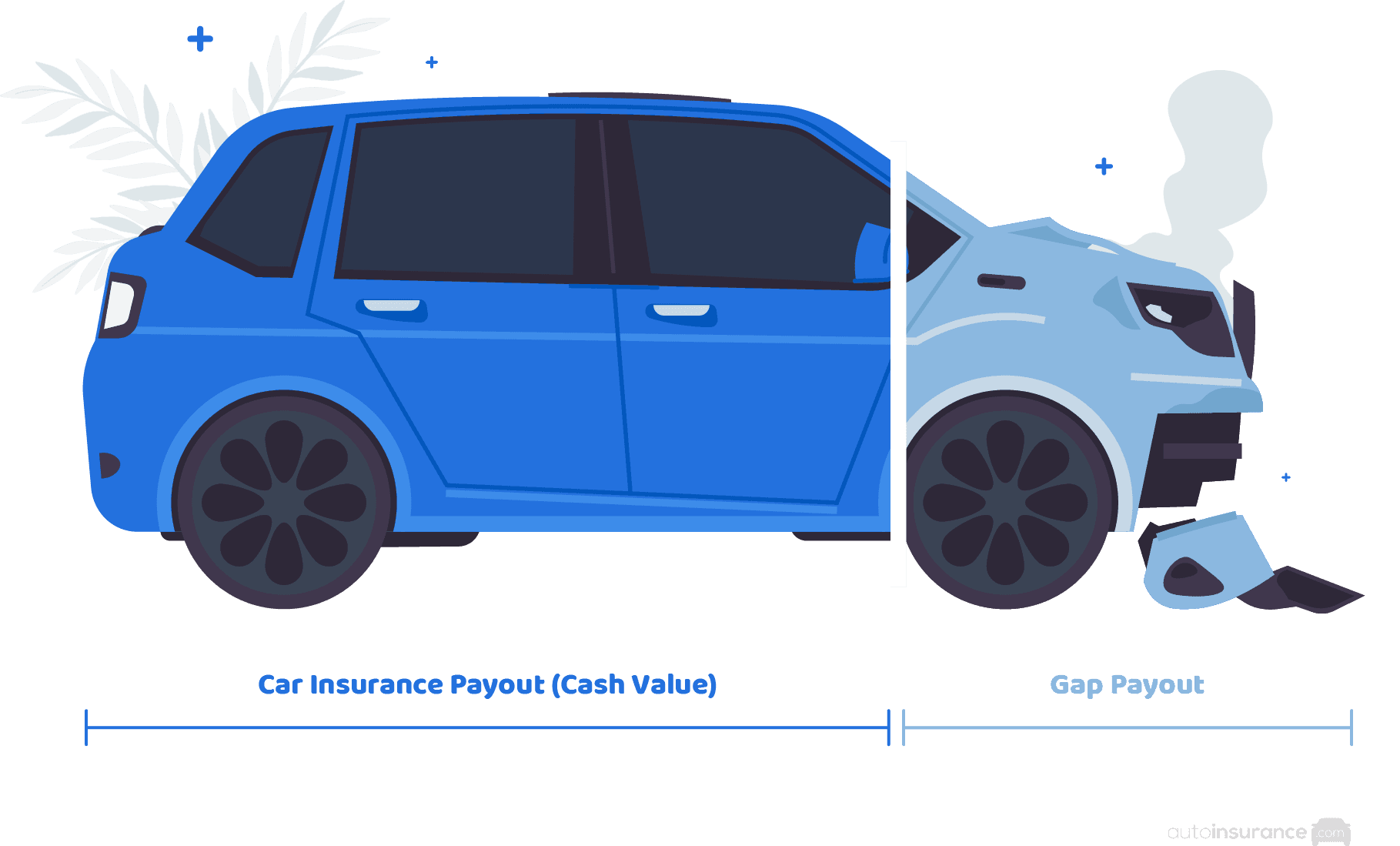

Gap insurance covers the difference between what you owe on your vehicle and its actual cash value if it’s totaled or stolen, protecting you from financial loss.

Get quotes from providers in your area

Summary:

- A new car typically depreciates in value the moment you drive it off the lot. Gap insurance pays the difference between your loan balance and your car’s actual cash value if it’s totaled or stolen.

- It’s ideal for drivers who made a small down payment, have long loan terms, or own cars that depreciate quickly. Your lender may require you to have it.

- You can usually buy it from your insurer, a lender, or a stand-alone provider—though dealerships often charge the most.

- It typically costs $20–$40 per year when added to an insurance policy.

What Is Gap Insurance?

In the event of vehicle total or theft, auto insurance policies pay out the actual cash value (ACV) of a vehicle at the time a claim is made. However, if you financed your vehicle, your settlement may not cover the amount you still owe. Gap insurance — which stands for “guaranteed asset protection” — covers the difference between the insurance payout and what you owe on the lease or loan.

FYI

“Totaled” usually means the cost of repairs is higher than what the vehicle is worth. In some states, a vehicle is a total loss if the cost of repairs is a certain percentage (e.g., 70 percent) of the car’s value.

In other words, because cars depreciate in value over time, your car may be worth less than what you owe at the time of an accident or theft. That could leave you with a big bill. Gap insurance protects you financially in this situation.

Does gap insurance cover theft?

Yes, gap insurance typically covers theft if your car is stolen and declared a total loss. Note that it only applies if your comprehensive insurance covers the theft and the vehicle isn’t recovered.

How do you know if you have gap insurance?

To find out if you have gap insurance, check your auto loan or lease agreement and your car insurance policy documents—gap coverage may be included by your lender or purchased through your insurer. You can also contact your lender or insurance company directly to confirm. If you bought your car recently and financed most of it, gap insurance is more likely to be in place.

Do I Need Gap Insurance?

According to the Insurance Information Institute, you should consider gap insurance if you:

- Put down less than 20 percent when you financed the car.

- Financed for five years (60 months) or more.

- Leased your vehicle (you’re often required to have gap insurance with a lease).

- Bought a vehicle that loses value faster than the average, like a luxury car.

- Rolled over negative equity from an old car loan into the new loan.1

If you own your car outright, you do not need to purchase gap insurance. If you financed a vehicle, and are “underwater” or “upside down” on your auto loan — meaning the market value of the car is less than what you owe — it’s a good idea to consider gap insurance.

How do you know if you’re underwater?

- Find your car’s value by entering your vehicle’s year, model, mileage, location, condition, and accident history on the Kelley Blue Book website or the National Automobile Dealers Association’s website.2 There’s no single, objective source for a car’s value, because prices fluctuate due to factors such as industry developments and economic conditions.

- Determine your loan balance by subtracting what you’ve already paid toward the loan from the original total loan amount, accounting for interest.

- Compare the value of your car to your outstanding loan balance. If the value of the car is less than the loan balance, you’re underwater (this is also known as having negative equity).

TIP

Cross-referencing from multiple sources can help you get a better sense of your car’s worth.

If you took advantage of a dealership incentive (for example, a low down payment with three months “free”), you’ll likely be underwater for several months after you purchase your vehicle. Incentives like these often offer a low down payment and several months “free,” which can put you underwater for at least a few months.

Who Can Skip It?

If what you owe on your vehicle is less than what the vehicle is worth, you do not need gap insurance. In general, you can skip it if you:

- Own your vehicle outright.

- Put down at least 20 percent when you financed your vehicle.

- Plan to pay off your vehicle in less than five years (60 months).

- Own a vehicle that holds its value over time historically (for example, in 2025, for the eighth time in a row, Kelley Blue Book named Toyota the best resale value brand).3

How Gap Insurance Works

Let’s say you buy a new car. A month later, you get into an accident and total your car. At the time of the accident, you still owed $30,000, but the car was only worth $26,000.

You have a $500 insurance deductible, after which your collision car insurance coverage pays you the value of the car at the time of the accident. So, after the deductible, your insurance pays $25,500. But you’re still on the hook for $4,500.

Gap insurance helps you pay that difference. Typically, it does not cover the deductible. But occasionally, some gap policies cover the deductible too.

Here’s a breakdown of how gap insurance works, using that example scenario:

| Factor | Amount |

|---|---|

| The amount owed at the time of the accident | $30,000 |

| Value of the vehicle at the time of the accident | $26,000 |

| Deductible | $500 |

| Insurance collision coverage pays | $25,500 |

| With gap insurance, the driver pays | $500 (deductible) |

| Without gap insurance, the driver pays | $5,000 (deductible + gap) |

Keep in mind that gap insurance only pays toward the balance of the loan. If you need to replace your car, consider adding new car replacement coverage to your insurance policy.

Where’s the Best Place to Buy Gap Insurance?

Gap insurance can be purchased through your existing auto insurance provider, car dealerships, banks or credit unions, or a gap insurance provider. Typically, dealerships offer significantly more expensive gap insurance than auto insurers, financial institutions, or a stand-alone provider.

See if your insurance company offers gap insurance as an add-on to your current policy. Companies like Liberty Mutual, Nationwide, Travelers, and Erie made our list of recommendations for the best gap insurance providers.

Keep in mind that most providers require you to have both collision and comprehensive coverage before you can purchase a gap policy (often, your lender requires these coverages, too). If your insurance doesn’t offer gap coverage, you may be able to buy it online from a stand-alone gap insurance provider. If you lease your car, check the terms of your lease — the dealership may include it automatically.

GOOD TO KNOW

Buying gap insurance from a dealership is typically the most expensive route. If you did buy gap insurance from your dealership and want to switch to a provider, you may be able to remove it from your contract.

Can You Buy Gap Insurance After You Get a Car?

Typically, gap insurance is only available when you purchase a new car, and you need to get it within three years of purchasing the vehicle.

That said, different insurers have different requirements and criteria for who can purchase gap insurance. Some insurance companies require you to be the first owner of the vehicle, that you buy gap insurance at the same time you purchase the vehicle, or that the vehicle be no more than two or three years old.4 Check with your provider for their policy on gap insurance.

How Much Is Gap Insurance Per Month?

Gap insurance purchased through a dealership can cost anywhere from $500 to $700. Gap insurance purchased through an auto insurance provider typically adds $20 to $40 to your annual premium. The exact cost depends on certain factors, like the value of your car at the time you purchased the policy, your age, where you live, and your claims history.

Dealerships or lenders typically charge an upfront flat fee for gap insurance. It may also be added into your loan, in which case you’ll also be charged interest.5 If you can’t get gap coverage from your insurance provider, a credit union will often be cheaper than a dealership.

What Does Gap Insurance Actually Cover?

In the unfortunate event that you get into an accident or someone steals your new car, gap insurance can help. But it doesn’t cover everything.

What It Covers

that most insurers require you to have both collision coverage and comprehensive coverage to purchase gap insurance. In the case of theft, you’ll need comprehensive coverage for the insurance to pay you the actual cash value of the car.

What It Doesn’t Cover

Gap insurance usually doesn’t cover:

- Insurance deductibles: Typically, gap insurance does not cover your deductible, although some policies might. Let’s say you have a $500 deductible on your collision coverage, after which your insurance pays out the value of the car. Gap insurance will help you cover the difference between the actual value of the car and what you owe on the loan, but it won’t go toward the $500 deductible.

- Missed loan payments or late fees: Gap insurance does not cover the cost of any missed loan payments or late-payment fees on your lease.

- Mechanical issues: Like standard auto insurance, gap insurance does cover losses from mechanical issues such as engine failures.

- Bodily injury and related costs: Damages such as bodily injury, medical expenses, lost wages, or funeral costs are not covered by gap insurance.

Is Gap Insurance Worth It?

If your car is worth less than what you owe, even if only for a few months, gap insurance is probably a good idea. That’s especially true if you wouldn’t be able to afford to pay off your loans in the event of an accident or theft.

In general, you can drop gap insurance after you’ve owned the vehicle for two to three years. By then, you should owe less on the loan than the vehicle is worth. When in doubt, check your loan balance against the current estimated value of the car.

Gap Insurance vs. Collision Coverage vs. Comprehensive Coverage

The table below shows the protection typically offered by gap insurance, collision coverage, and comprehensive coverage, as it relates to financed vehicles:

| Coverage Type | What it Covers |

|---|---|

| Gap insurance | The difference between the payout from collision and comprehensive coverage, and the amount still owed on your financed vehicle |

| Collision coverage | Damages sustained while your vehicle is in motion, such as in a car accident |

| Comprehensive coverage | Damages not related to driving, including theft, vandalism, falling objects, and weather-related damage |

Pros and Cons of Gap Insurance

Pros

Financial protection: If something happens to your new car, gap insurance covers the difference between the vehicle’s value and what you owe in loans. This could mean avoiding thousands of dollars in bills at an already stressful time.

Usually affordable: When you buy gap insurance through your current auto insurance provider, it usually adds only a few dollars per month in premiums.

Peace of mind: Gap insurance can offer peace of mind, especially if you own a car that depreciates in value quickly.

Cons

Can be expensive: Gap insurance is not available through all insurance providers. Purchasing a gap policy from a dealer or lender can be pricey.

Limited protection: If something happens to your vehicle, gap insurance does not give you money to put toward a new one.

Only available for new vehicles: You usually can’t get a gap insurance policy when you purchase a used car.

Alternatives to Gap Insurance

If gap insurance doesn’t work for your situation—or you’re buying a used car that doesn’t qualify—there are several alternatives. Each has different eligibility rules and coverage amounts.

Loan/Lease Payoff Insurance

Some insurers use the term “loan/lease payoff insurance” interchangeably with “gap insurance.” Loan/lease payoff insurance is often available for used cars where gap insurance is not, and typically covers 25 percent of the actual cash value of the vehicle. Progressive is an example of a company that offers this coverage.

Let’s say you paid $40,000 for your truck, and someone steals it a month later. In that time, the value of the truck depreciated to $30,000. Loan/lease payoff insurance will pay you 25 percent of the truck’s value, which is $7,500. While loan/lease payoff doesn’t cover the remainder of a loan like gap insurance does, it usually covers the difference or close to it.

New Car Replacement Insurance

New car replacement insurance helps you pay for a new car (minus the deductible) to replace your former vehicle should something happen to it. Typically, new car replacement insurance costs more than gap insurance. It’s a good choice if you’re more concerned with the cost of buying a new car than the outstanding balance of your current loan.

Better Car Replacement Coverage

In the event of total vehicle loss, better car replacement coverage gives you money to purchase a newer model with fewer miles.6 For example, Liberty Mutual offers money toward a vehicle that is one model year newer with 15,000 fewer miles. Better car replacement coverage is a good option if you buy a used vehicle, which often isn’t eligible for new car replacement or gap insurance.

Recap

Depending on how you financed your new vehicle, it may be worth less than what you owe. When you’re “underwater” on your auto loan, gap insurance is often a good idea. Your car insurance provider, bank, or credit union will often have cheaper gap insurance than a dealership.

Frequently Asked Questions

The best place to buy gap insurance is your current insurance provider, a stand-alone gap insurance company, or a credit union. Your dealership or lender may offer to sell you gap insurance when you buy a new vehicle, but this option typically costs more.

When you add gap insurance to an existing auto policy with collision and comprehensive coverage, it typically adds only a few dollars to your monthly premium, or about $20 to $40 annually. Gap insurance costs more through a dealer or lender. Usually, you’ll pay a flat fee of $500 to $700, or the dealer/lender will add gap insurance to your loan and you’ll pay additional interest.

Gap insurance coverage is usually worth it for any period of time when your car is worth less than what you owe, especially if you can’t afford to pay the difference in the event of an accident or theft. In general, you don’t need it if you put at least 20 percent down when you finance your vehicle. You can usually drop it after you’ve owned the car for two to three years; by then, you should owe less than what it’s worth.

You’re “underwater” on your auto loan if what you owe is more than the value of your car. You can find your car’s value by checking websites like Kelley Blue Book, Edmunds, or the National Automobile Dealers Association.

There’s no single, objective source that determines your vehicle’s value, so check around. Compare the value of the vehicle to your outstanding loan balance. If the vehicle is worth less than the loan balance, you’re underwater.

No, gap insurance won’t cover your car if you total it while under the influence of drugs or alcohol. Most providers exclude accidents caused by DUIs in gap insurance policies, so you’ll be responsible for the difference between the amount you owe and the actual value of the car at the time of the accident.

Citations

What is gap insurance? Insurance Information Institute. (2024).

https://www.iii.org/article/what-gap-insuranceConsumer Vehicle Values. National Automobile Dealers Association. (2024).

https://www.nada.com/2024 Best Resale Value Awards: Top Cars, Trucks and SUVs. Kelley Blue Book. (2024).

https://www.kbb.com/best-cars/best-resale-value-cars-trucks-suvs/What Is Gap Insurance And How Does It Work? Allstate. (2024).

https://www.allstate.com/tr/car-insurance/gap-insurance-coverage.aspxWhat’s UP with Gap Insurance? United Policyholders. (2024).

https://uphelp.org/buying-tips/whats-up-with-gap-insurance/What is Better Car Replacement™? Liberty Mutual Insurance. (2024).

https://www.libertymutual.com/vehicle/auto-insurance/coverage/better-car-replacement

Related Articles

Farm Bureau Car Insurance Review 2026

March 31, 2026Best Cheap Car Insurance in St. Petersburg

March 31, 2026