Last updated: September 24, 2024

Guide to Insurance for New Cars

Protect your new ride with the best coverage for you.

Get quotes from providers in your area

Depending on where you live, you must have auto insurance or proof of financial responsibility before you drive a new vehicle off the lot. You will be accountable for accident damages no matter where you drive, so it pays to stay covered.

Before you insure your car, make sure you understand your coverage needs and your budget. Learn where to start by reading our strategy for insuring your new car.

Find out if you're overpaying for auto insurance.

See how much you could be saving! Let's get started by entering your ZIP Code:

Video Breakdown

How Auto Insurance Works When Buying a New Car

You can buy a car without insurance, but in most states, you won’t be able to drive it off the lot until your car is insured. Even if your state doesn’t require it, auto insurance protects you from paying out of pocket for the full cost of an accident.

You have two options when insuring a new car: You can sign up for a new policy or transfer your existing policy to cover your new vehicle. With insurance coverage, you can file a claim in the event of an accident.

Starting a New Policy

If you choose to start a new policy, shop around to find the best coverage within your budget. Even if you haven’t picked a make or model yet, you can get an insurance quote on your potential car purchase.

If you choose to get a car insurance quote, find out your state’s minimum coverage requirements and your desired coverage. It is smart to request at least three quotes from different companies. Use the same information for each request to make it easier to compare rates directly and choose the right match for your new vehicle.

NOTE

You should know your vehicle identification number (VIN) when applying for new coverage to speed up the quoting process.

If you are looking to start a new policy, compare policies in detail. Going over your options for coverage, limits, and deductibles is just as important as comparing rates.

Find out how your potential insurer handles claims. Customer service with 24/7 availability and quick responses will improve the claim-filing process. The easiest way to find information on a company’s service is to check customer satisfaction ratings with an accredited rating agency like J.D. Power1.

Adding a New Car to an Existing Policy

If you are transferring an existing policy, all you need is proof of insurance to drive your car off the lot. Insurance companies offer a grace period of seven to 30 days to adjust your policy after you purchase a new vehicle2. The grace period allows you to reassess your coverage needs and update your budget. It helps to reassess your policy at least once a year to ensure your needs are met without paying for additional coverages.

TIP

If you are switching policies, make sure your new policy is in effect before you cancel your current policy. You never want a lapse in coverage, because if you get in an accident without insurance, you will have to pay out of pocket for any losses and could face legal ramifications.

Using Your Policy

Once you begin a new policy or transfer an existing one, you can file a claim in the event of an accident. A claim is a formal request to your insurance company for money to help with accident expenses. If damages cost less than your deductible, filing a claim is not worthwhile. You can only receive a claim payout after you pay your deductible in full3.

Most insurance companies give you the option to file claims online or with insurance agents, either by phone or in person. After filing a claim, an insurance adjuster may investigate the information you provided to get the clearest picture of what happened. The adjuster will then make a recommendation for how much the insurance company should pay you for the loss or losses.

Auto Insurance Coverage You Need

Regardless of how you purchase a new car, you must meet your state’s minimum insurance requirements. While these requirements differ by state, below are some of the coverages you can expect to need.

- Liability coverage: Liability coverage covers damage or injuries to other parties in accidents where you are at fault.

- Uninsured/underinsured motorist coverage: When an uninsured or underinsured driver hits you, uninsured motorist coverage (UM) and underinsured motorist coverage (UIM) take care of your expenses4.

- Medical payments coverage or personal injury protection: Medical payments coverage (MedPay) pays for your and your passengers’ medical expenses that result from car accidents. MedPay is only available in at-fault states. Personal injury protection (PIP), on the other hand, includes medical payments coverage but covers other documented losses, such as lost wages and child care costs. PIP is only available in no-fault states like Florida.

Other insurance coverage requirements depend on whether you are buying, leasing, or financing a new car.

Buying a Vehicle

If you are buying your car outright, you only need to meet your state’s minimum coverage requirements.

Leasing a Vehicle

When you lease a vehicle, you pay to drive it for a specified period. Once your lease ends, you either renew the lease, return the car, or buy it.

Since you don’t actually own a leased vehicle, the lessor may require more coverage than the mandatory minimums, such as comprehensive and collision coverage, until you complete the payments. Whether or not you are at fault in an accident, collision coverage will cover damages to your vehicle. Comprehensive coverage covers all other damages not related to collisions like vandalism or auto theft.

Additionally, a leasing company may have a minimum deductible amount you must meet while paying off your vehicle. Since higher deductible payments often lower premium costs, the minimum deductible will increase your monthly costs5.

Financing a Vehicle

Financing a vehicle is similar to leasing, but instead of paying to drive a car, you pay to own it. A bank or dealership may require certain insurance limits for a financed car. These limits ensure you have the means to keep paying your loan if you get into an accident.

Your financing terms won’t change if your car is damaged, but you will still be responsible for loan payments. You could benefit from gap insurance while financing a car: If the car is totaled, gap insurance will pay the difference between what you owe on a vehicle and its actual cash value6.

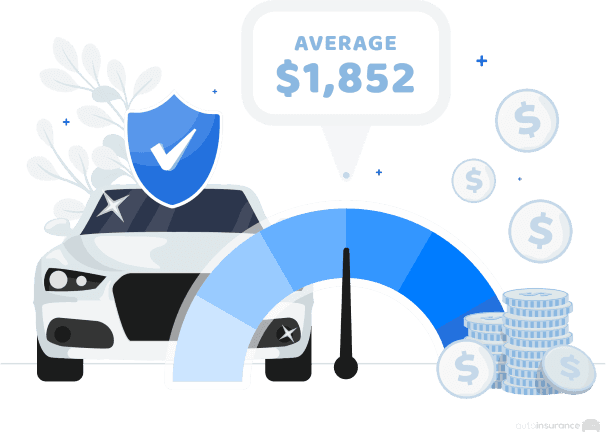

The Cost of Insuring a New Car

The average cost to insure a new car is $1,852 annually. Your rates for insuring a new car may be more or less than the average, depending on your driver profile and prospective car purchase, however. Auto insurance rates depend on these factors:

- Make and model

- Model year

- Title and damage history

- Mileage

- State and ZIP code

- Deductibles

- Age

- Marital status

- Homeownership

- Your driving records, including any at-fault accidents

- Coverage options (i.e., the more coverages you get, the higher your rates)

- Provider (different car insurance companies charge different rates for similar products and services)

- Gender (except in California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania)

- Credit score (except in California, Hawaii, Michigan, and Massachusetts)

Vehicles will have cheaper insurance rates if they have low repair costs, strong safety records, or anti-theft features.

FYI

When you purchase new auto insurance coverage, you should list on your policy all the people who drive your vehicle regularly. Most insurance companies want all licensed drivers in your household to be on your policy so they can calculate your rate accurately.

Dealer Insurance

It is a dealership’s responsibility to insure its vehicles in the event of possible damages, not your responsibility as a potential buyer7. However, dealer insurance only covers test drives, so you will not have protection once you buy the car.

Recap

Whether or not your state requires auto insurance, you can protect yourself against damages by insuring your new vehicle. Stay up to date on your state’s minimum requirements and reassess your policy annually to avoid overpaying for coverage you don’t need.

Frequently Asked Questions

If you total a brand-new car, you will face all damage charges unless you have collision coverage. If you do have collision coverage, your auto insurance company will pay the actual cash value of your car minus your deductible. If you are financing your car, you may end up owing more money than the car is worth with the damages. Unless you have gap insurance, you will still be responsible for paying what you owe on the car.

Usually, insuring a new car is more expensive than insuring a used car, but this rule of thumb becomes tricky when you factor in the make and model of a vehicle.

A car is a depreciating asset: The more you use it, the less it is worth. If you use a new car frequently, the cost could be similar to insuring an older car you have yet to use.

In general, newer cars have better safety ratings and are easier to repair, but they also cost more to replace. Your monthly payment may be higher for a newer vehicle, but your overall costs will be lower.

Many other factors beyond whether your car is new or used contribute to your policy’s cost, such as your driver profile and your coverage choices.

Citations

Auto Insurance Customer Satisfaction Stalls Despite $18 Billion in Premium Relief, J.D. Power Finds. American Family Insurance. (2021, Jun).

https://www.jdpower.com/business/press-releases/2021-us-auto-insurance-studyNew car insurance. Progressive. (2022).

https://www.progressive.com/answers/new-car-insurance/How to File an Insurance Claim: Everything You Need to Know. Ramsey. (2022, May).

https://www.ramseysolutions.com/insurance/how-to-file-an-insurance-claimUninsured and underinsured coverage: Protection from unprotected motorists. Allstate. (2020, Nov).

https://www.allstate.com/resources/car-insurance/uninsured-motorist-coverageLeasing Vs. Buying A Car: 9 Questions To Ask. Geico. (2022).

https://www.geico.com/living/saving/money/car-leasing-vs-buying/What Happens When a Car Is Totaled?. American Family Insurance. (2022).

https://www.amfam.com/resources/articles/on-the-road/what-happens-if-your-car-is-totaledAuto & Truck Dealers Insurance. Travelers. (2022).

https://www.travelers.com/business-insurance/auto-dealer

Related Articles

The Safest Cars According to Insurance Loss Data

March 10, 2026Why is Car Insurance So Expensive in New York?

March 5, 2026Best Cheap Car Insurance in New York City

February 24, 2026